Subscribe for cutting-edge B2B tech research.

See Value Better

Spear is a fundamental asset manager focused on industrial technology. We help you do more than passively track the broader market.

Networking Cornucopia

It was a busy week for tech earnings with outsized moves in Networking and Cybersecurity. Here is everything you need to know:

🔌 Networking — The next leg of the AI hardware trade

- Marvell — The pieces of the puzzle are coming together

🔓 Cybersecurity inflection on the horizon

- Crowdstrike vs. SentinelOne — the impact of the incident

- Zscaler — addressing the billings conundrum

Our weekly digest is intended to keep you on the cutting edge of investments in data infrastructure, software and cybersecurity.

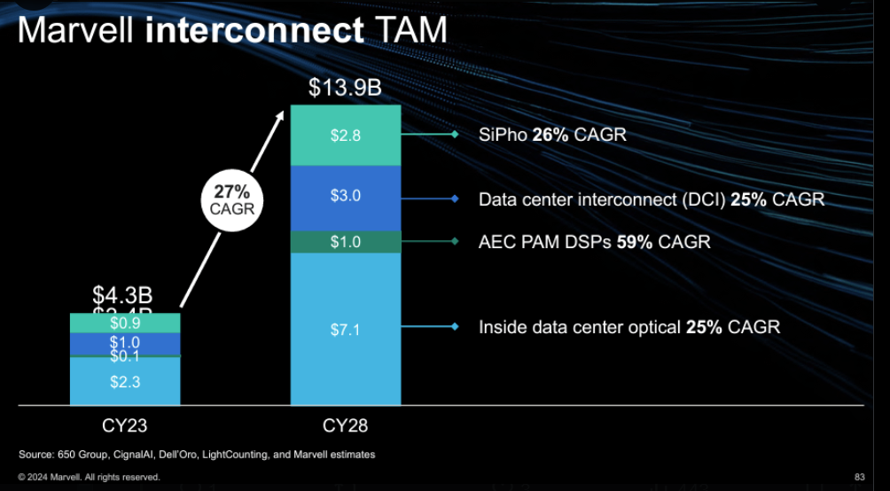

| Networking is the Next Leg of the AI Hardware Trade In the inaugural issue of the Tech Edge, we highlighted the implications of Nvidia earnings for networking and broader data center build-out LINK. Marvell, a networking leader, reported just that. For background, Marvell is a leader in interconnects, a sub-category of networking, and over the past several years, it has expanded into custom chips. Custom chips and networking are two of the most attractive areas of data center hardware as we look into ’25. Custom Chips (ASIC). Nvidia has established a leadership position in AI chips, with some estimates of a 90%+ market share. Nvidia’s largest customers, the cloud service providers, want a piece of the pie. All three major hyperscalers, Amazon, Microsoft, and Google, are designing their own chips with the help of 3rd party providers such as Marvell and Broadcom. Amazon has been making a significant push on the custom side with its Trainium chips. The company recently announced an intention to build a large data center using its own chips in ’25, with Apple as a key customer. Marvell was highlighted as one of the key partners. Not surprisingly, Marvell reported a blowout quarter, exceeding F3Q25 expectations and guiding to Data Center growth of low-mid 20s QoQ (vs. Street at 11%) largely driven by ASICs. ⬆️ The company previously provided an AI guide of $1.5B in ’25 and ~$3B in ’26 and can exceed both by a few hundred million; AI is further expected to ramp to ~$8B for ASIC and ~$8B for Networking by ‘28…which management was committed to.🚀 The Amazon partnership largely drives the upside for ‘25, But Marvell highlighted that Customer 3 (a.k.a. Microsoft) is expected to be potentially bigger, ramping in ‘26! 😳 Networking. On the networking side, Marvell is a leader in interconnects, which grow at multiples of accelerator growth levels. ✖️✖️✖️ The company expects AI networking to grow double-digit QoQ (vs. Street at 11%). ⬆️ Moreover, Marvell is expanding to several adjacencies with multiple $B TAMs. The most significant are: 1. AEC interconnects2. DCI3. Switches4. PCIe …all expected to grow higher than the overall Networking business. All of the above were cited as being part of the Amazon deal. The particularly attractive part about networking is that while there are many players, they each specialize in different areas. Arista and Broadcom (and now Nvidia) have a significant presence in Switches, Marvell and Broadcom are leaders in interconnects, etc. This market structure allows for high and sustainable margins and returns. |

| Cyber Inflection on the Horizon Most cybersecurity companies that reported earnings delivered underwhelming results (excluding hardware, which follows a different cycle). Meanwhile, cyber threats are at an all-time high. So what is going on? 😕 Our take is that the market is focused on the wrong metrics (revenue & billings), while forward-looking metrics such as Net New ARR and growth from new products are telling a different story and inflecting upwards. For SaaS companies, the impact of a cycle gets smoothed out over several years. While metrics have been looking okay over the past two years despite very tight enterprise spending, revenue and billings growth have been impacted by slower business conditions over the past 1-2 years. Thoughts by company on the reported earnings: Crowdstrike – Solid earnings but starting to feel the impact of the incident, albeit much less than people expected 😐Cloudflare – The guide was slightly disappointing at the time of the report, but looks great compared to the rest that were reported later😃Zscaler – Billings guide in the teens for 1H is throwing people off, but fundamentals are much stronger than that datapoint implies (see Zscaler section below) 💡Datadog – decent report with AI Native Products ramping 🚀Palo Alto – Solid NGS performance, but valuation in question 😐SentinelOne – Re-accelerating NNARR, but investors were expecting a bigger benefit from Crowdstrike ❓Okta – strong quarter but guiding to only 7% revenue growth for F26 😐 |

-1.png?upscale=true&width=1120&upscale=true&name=Cybersecurity%20Overview%20(8)-1.png)

| In terms of valuations Crowdstrike and Cloudflare trade at the highest multiple, reflective of the quality of the platforms. Zscaler screens very attractively if they can deliver (which people seem to be doubtful of). SentinelOne and Okta trade at the lowest multiples reflective of growth concerns. Both companies don’t meet the Rule of 40 and need to re-accelerate growth to work. |

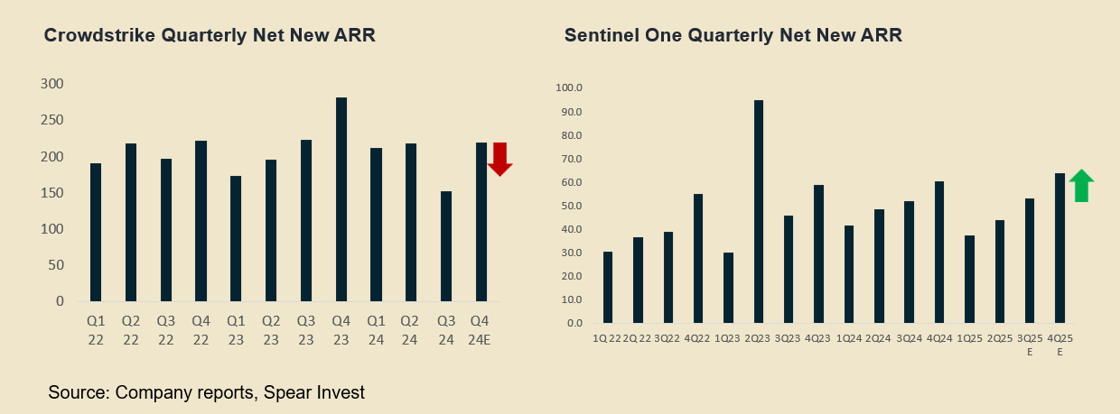

| Crowdstrike vs. SentinelOne Incident Impact Crowdstrike is holding it together, but the incident is starting to show up in the numbers. Coming out of both company earnings calls, the conclusion is that the impact will likely be less severe than many feared but will also be more prolonged. This is reflected both in the Crowdstrike guide for NNARR, which now the company expects to re-accelerate in 2H25 vs.1H25 implied at FalCon, and SentinelOne management commentary that the impact is positive for the pipeline and value proposition vs. and less of a one-quarter impact. This is because cybersecurity sales cycles are long (6 months+), and companies don’t replace vendors on a whim. In the quarter, Crowdstrike showed a small downtick in Gross Retention Rate (less than .5%,) and SentinelOne pointed to a handful of deals won as a result of the incident (a Fortune 50 company and several government contracts). Investors expected a bigger impact than this. Both companies are showing very strong momentum in new products, which we believe will power the next growth cycle: Crowdsrike showed strong momentum in SIEM – ARR up >150% yoy on a solid base 🚀 SentinelOne highlighted $170M in business in Cloud and Data Security/SIEM.Purple AI attach rates double QoQ 🚀This translates to NNARR acceleration for SentinelOne, returning to growth at +4% YoY(+22% QoQ ) – the strongest sequential growth since FY21. But a more muted impact for Crowdstrike due to the incident. |

| Zscaler — The Billings Conundrum 🤔 As evident from the abovementioned valuation discrepancy, investors don’t believe in Zscaler’s forward numbers. Here is what’s causing the confusion: For background, Zscaler is a leader in “zero trust” security and has a unique platform that has been growing revenues and billings in the mid-high 20%s. All of a sudden, as of two quarters ago, the company guided to depressed billings growth in ‘F1H25 in the low teens 😮 and a recovery in 2H to the mid-high 20%, which nobody believes. Not surprisingly, everyone is panicking because no one wants to pay >10x revenue for a company that grows in the teens. The company has also said that billings are the best metric to track the business, but this is only correct if investors understand how the metric works. Here is the key – billings are impacted by business done in the prior year(s). Consequently, Zscaler has very good visibility in scheduled billings — which is the metric in question. Consequently this is less of a ramp and more mechanical impact of when deals were done. Unscheduled billings, which is business done in the quarter (new, upsell and renewal billings) were actually growing over 20%. We think this is the key metric to track. In summary, cybersecurity business trends are solid, emerging areas such as data and cloud security are booming, but it will take some time for metrics such as revenues and billings to return to prior growth levels as they need several years of strong growth to build on. |