Subscribe for cutting-edge B2B tech research.

See Value Better

Spear is a fundamental asset manager focused on industrial technology. We help you do more than passively track the broader market.

Beyond the numbers: Nvidia’s results and the DC Value Chain

Nvidia’s results and the DC value chain:

😫 What is causing investors to panic?

🗒️ Five key takeaways from the call

🌐 Implications for the value chain

📈 When the VIX spikes, it’s time to buy!

In this week’s Tech Edge, we dive into Nvidia’s earnings and its implications for the rest of the Data Center value chain.

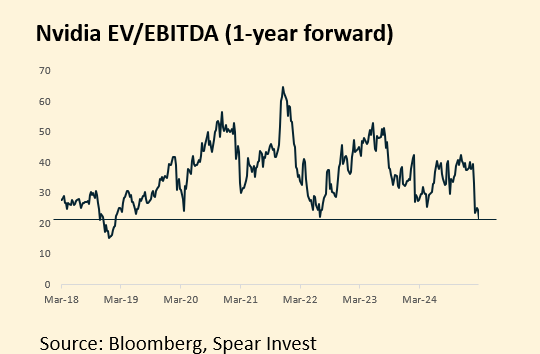

| Our weekly digest is intended to keep you on the cutting edge of investments in data infrastructure, software, and cybersecurity. 😫 What is Causing Investors to Panic Nvidia reported its F4Q25 earnings ahead of their guide and Street expectations.Revenue for the reported quarter came out at $39.3B which exceeded the guide of $37.5B and Street expectations by ~$1B. Similarly, the guidance for the upcoming quarter F1Q26 came out at $43B, also ~$1B better than the Street. Blackwell, the company’s new chip, contributed $11B to the current quarter beating Street expectations of $5-6B. Why did investors not like this 🤔?Less than usual beats. Despite the Blackwell beat of $5B, overall revenues did not surprise by the usual $3-4B. Everyone is already nervous post DeepSeek and no huge beat and raise put the thesis on hold. Investors are also worried about tariffs, DOGE cuts, and slowing economic growth, adding to worries about the durability of the AI trade. What are people missing? Blackwell is a very different architecture with a significantly more complex supply chain. Everyone wants it because it offers significantly better price performance, but it’s not as easy to make. The stock will start working again when “Blackwell beats” move the overall needle. We expect that this will be in the next 1-2 quarters. Blackwell is likely to ramp from the current $11B to ~$200B, which is huge. The macro narrative could easily shift to tax cuts, re-accelerating economic growth, and productivity improvement as we look into the second half. In the meantime, Nvidia stock has a strong valuation support and rarely trades below 20x 1-year forward EBITDA. It is the only company in our coverage universe that trades near 20x EV/EBITDA and is growing revenues by 50%+ yoy 😲. |

| 🗒️Five Key Takeaways From The Call: Blackwell is the fastest product launch contributing $11B to the current quarter …this was way ahead of sell-side estimates of ~$6B and implies that the ramp could be huge in 2H25. Systems (e.g., GB200) will ramp significantly in 2H, which will drive gross margins back into the high 70s%; GMs are currently in the low 70s%. Blackwell Ultra, the next generation of chips coming later this year, is expected to have a very easy transition as it has a similar architecture to the current generation. Model types are broadening; this is positive for Nivida but also very positive for the rest of the value chain as different types of models require different infrastructure. Signs of a shift from InfiniBand to Ethernet. It’s not surprising as both have specific value propositions. Positive for the networking players. Investors should not miss the forest from the trees. While it may be taking Nvidia longer than some hoped to ramp Blackwell from $ Billions to hundreds of $ Billions due to complexity in the supply chain, demand is off the charts, with every cloud vendor significantly increasing capex. For more on this topic, tune into Yahoo Finance 👇 |

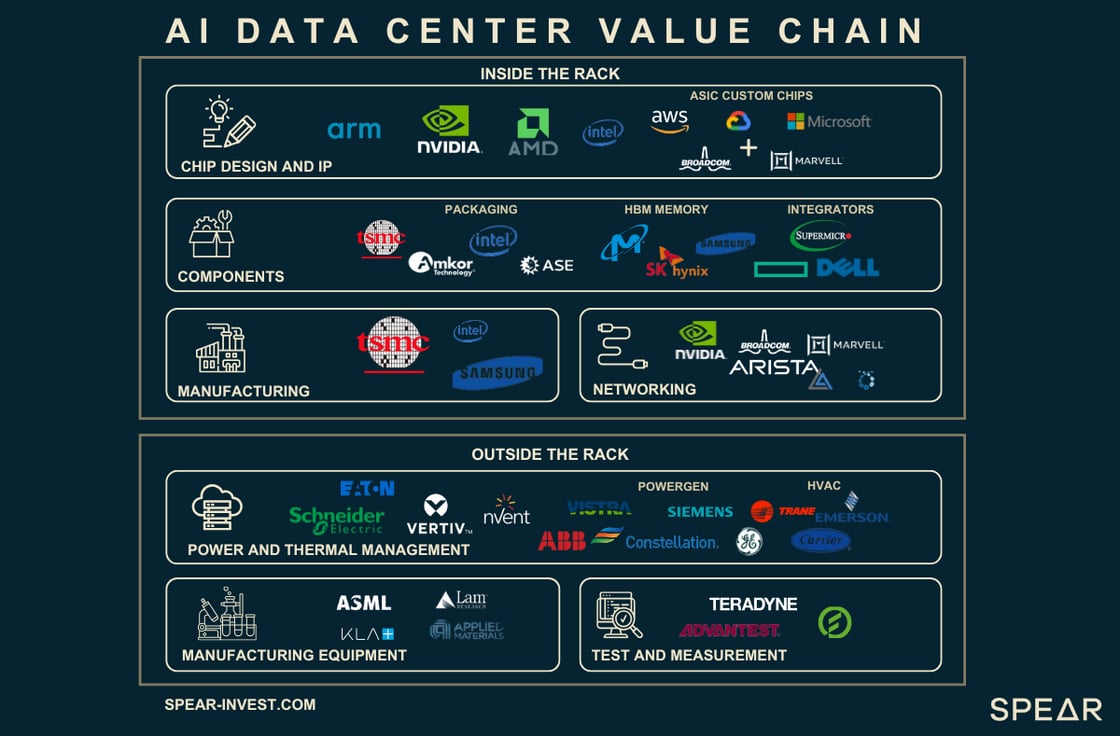

| 🌐The Rest of the Value Chain Despite the recent sell-off, Nvidia is actually holding up much better than the rest of the value chain. This is where we are finding most of the outsized opportunities, as many stocks are off 40%+ from early January. The fact that different use cases require specialized hardware is going to be very significant for the networking plays as users will customize their setups. For example, robotics & autonomous driving will be very model training intensive, where massive data centers will be required. On the other hand, Agentic AI will require “test time scaling” models, which will be optimized on different types of hardware and software infrastructure. |

| To learn more about the different areas and key players of the hardware value chain, tune into our on-demand webinar. |

| In conclusion, the market has started on shaky ground this year with people worried about tariffs, DOGE, economic growth, and uncertainty about the AI trade, but the focus could easily shift to tax cuts, re-accelerating economic growth, and productivity improvement as we look into the second half. When the VIX spikes it is usually a good time to buy! |